May 2025 CPI Forecast

Tomorrow at 8:30 am ET, we will get the long-awaited May CPI. Given the Fed’s hyperfocus on tariffs and their impact on inflation, May CPI could be a crucial input for the Fed’s rate policy over the next few months.

In Q1 2025, headline CPI printed at +0.2% MoM on average, which is -0.1 pp better than in Q4 2024. In Apr 2025, headline CPI came in at +0.2% MoM, -0.1 pp cooler than the market expected. This was the coolest Apr since the 2020 recession and the 2nd coolest Apr since 2017. The last 3 months came in -0.1 pp cooler than consensus expectations on average.

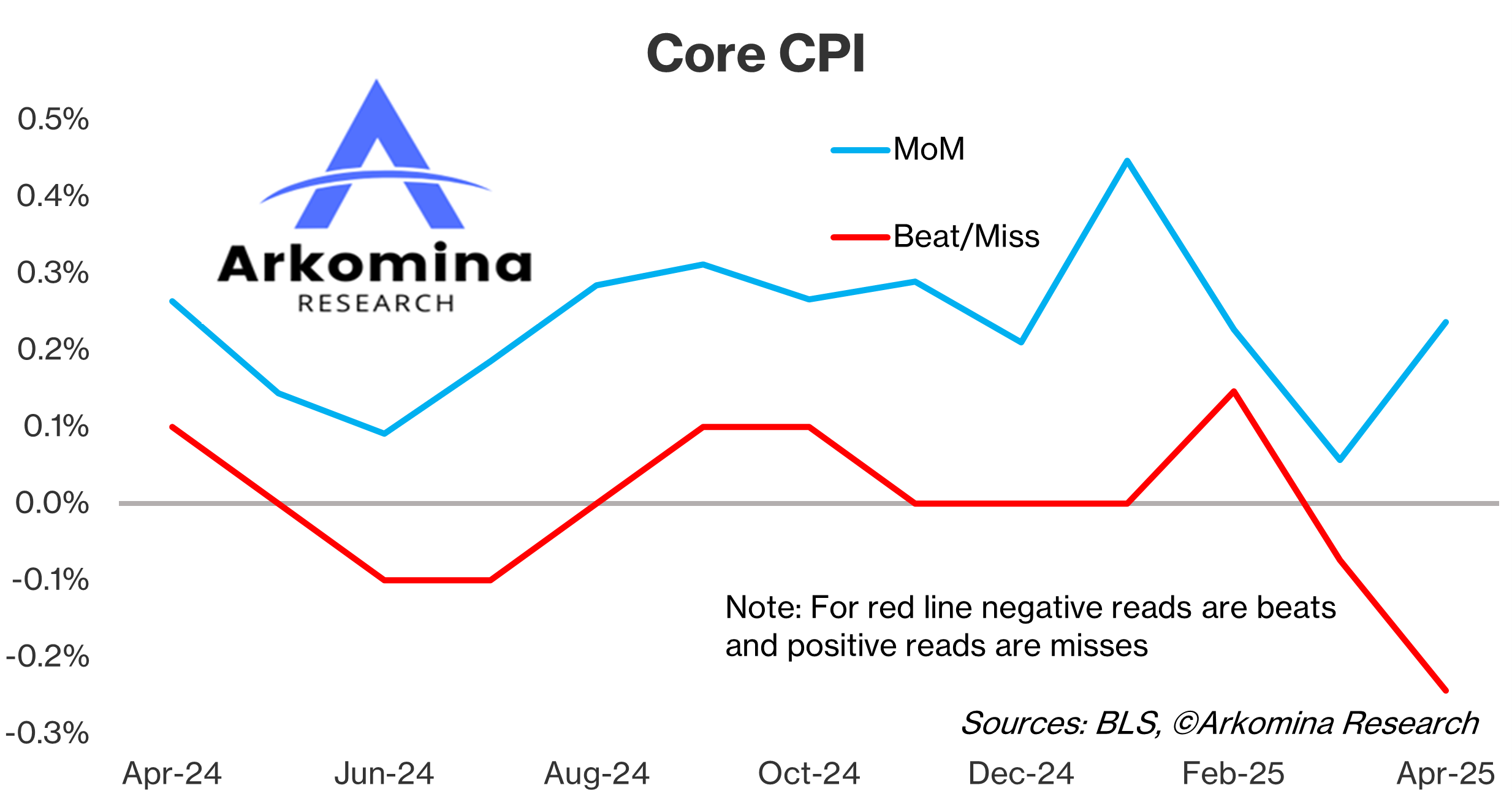

On average, core CPI in Q1 2025 was also +0.2% MoM, which is -0.1 pp below Q4 2024 average MoM figures. Core CPI at +0.2% MoM in Apr 2025 was also cooler than expected and the coolest Apr since the 2020 recession. The last 3 months were -0.1 pp cooler than consensus expectations on average. The crucial question is, can the cooler prints persist, or will tariffs increase CPI?

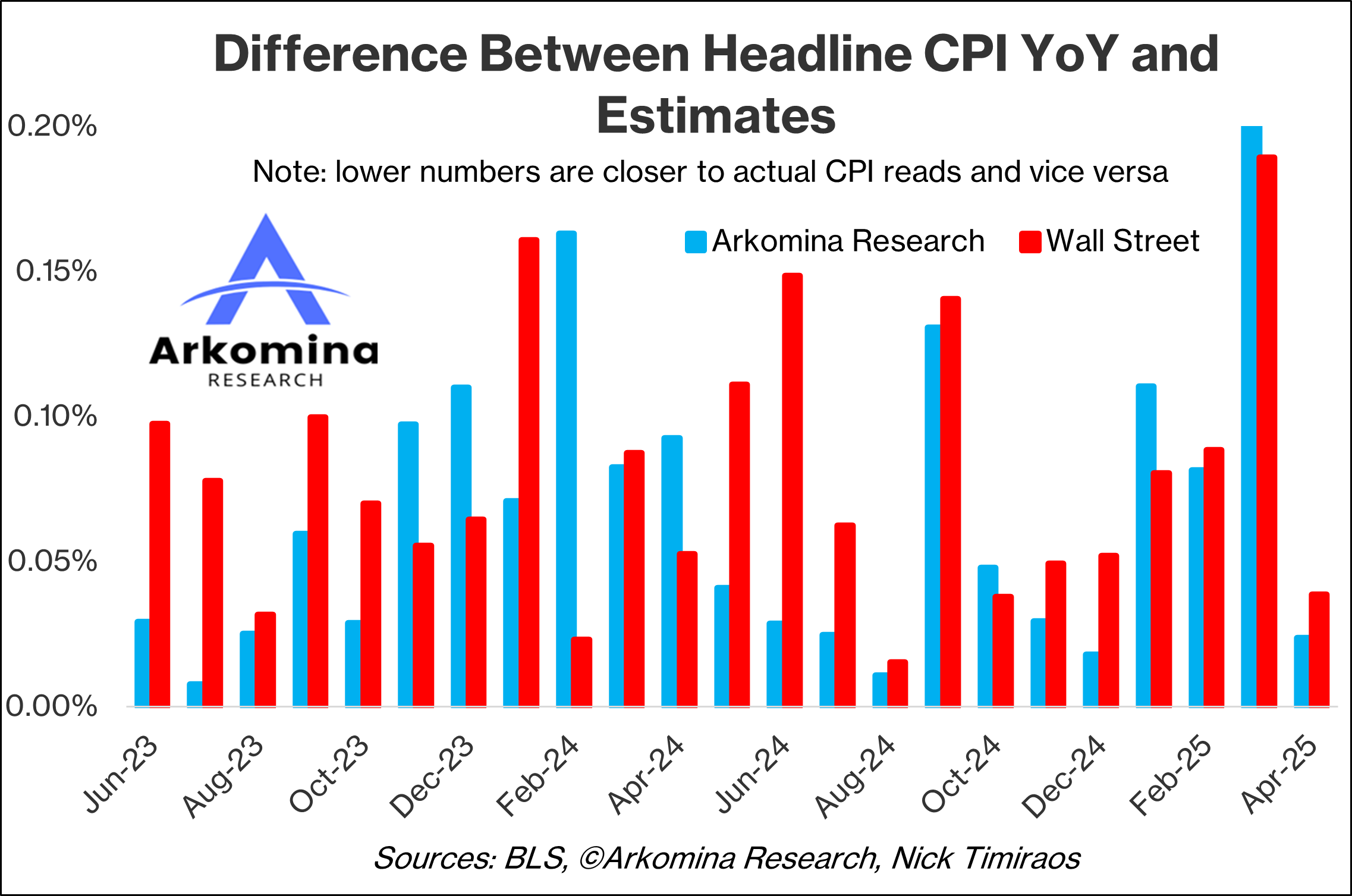

My average error for estimating headline CPI (based on the last 27 CPI estimates from Feb 2023 - Apr 2025) is almost perfect at -0.7 bps (-0.007 pp).

More importantly, my headline CPI estimates have been closer to the actual number than the average Wall Street estimates by 2 bps on average, 16 times in the last 23 months, or 70% of the time.

My average error for estimating core CPI (based on the last 27 core CPI estimates from Feb 2023 - Apr 2025) is almost perfect at -0.7 bps (-0.007 pp).

My core CPI estimates have been closer to the actual number than the average Wall Street estimates by 1 bps on average, 16 times in the last 23 months, or 70% of the time.

For public links to my prior CPI estimates, go to ArkominaResearch.com.

The Fed has expected a higher tariff-related inflation for months now, but so far, this hasn’t materialized in the CPI data. Is May a month when they will finally see hotter tariff-related prints, or will the cooler prints continue?

My May CPI estimates are…

Headline CPI

+0.1% MoM (-0.1 pp lower than consensus, and -7 bps below the Cleveland Fed)

+2.3% YoY (-0.2 pp lower than consensus and -6 bps below the Cleveland Fed)

Core CPI

+0.1% MoM (-0.2 pp lower than consensus and -11 bps below the Cleveland Fed)

+2.8% YoY (-0.1 bps lower than consensus and -8 bps below the Cleveland Fed)

My unrounded estimates:

If CPI comes in line with my estimates, I’d expect some to try and question the high tariff-related inflation expectations. Still, this may not be the ultimate evidence that these expectations have not materialized, and the Fed would likely seek more evidence to understand how tariffs are impacting inflation. That said, they are unlikely to cut next week, while what happens in Jul could depend on Jun inflation and (un)employment data.

Arkomina Research also offers a premium service, which is different from Substack. If you’re interested in learning my longer-term CPI estimates (4 quarters out), consider subscribing to Marko’s CPI Report, which goes out each month before CPI and, among other things, contains analyses of:

Comprehensive analysis of CPI data

Forward-looking inflation indicators

Detailed May CPI estimate

Headline and core CPI trajectory 4 quarters out

Preliminary Jun CPI estimate

To get Marko’s CPI Report, make sure to subscribe to Arkomina Research Pro Investor at this link: ArkominaResearch.com/Subscriptions/

By subscribing to Pro Investor, you also get:

Marko’s Brain Daily: Sent each trading day around 6 am ET, covering prior-day macro indicators and events (e.g., Fed speeches, meetings), daily estimates for key indicators with market reaction scenarios, short-term equity and bond market outlooks, plus earnings, tariff analyses, and more.

Marko’s Fed Report: Delivered before each Fed meeting and, among other things, includes analyses of what the Fed has done so far, what they will do at their next meeting, a detailed economic situation, analysis of monetary policy lags, predcitions about what the Fed will likely do over the next 4 quarters, and the unemployment rate and PCE inflation trajectories over the next 4 quarters.

DISCLAIMER

These articles are for discussion and educational purposes only.

Past performance is no guarantee of future results.

Although specific securities and economic forecasts may be discussed in articles, you should NOT construe any comment as a call to buy or sell any security or as legal, tax, investment, financial, or other advice. Consult your own advisors if you require such advice.

ANY USE OF THESE ARTICLES IS AT YOUR OWN RISK AND LIABILITY. Neither Arkomina Consulting Ltd nor Marko Bjegovic, as its director or any employee, accepts any liability whatsoever for any direct, indirect, consequential, moral, incidental, collateral, or special damages or losses of any kind.

Your inflation estimates have consistently been the best in the market